Weekly Markets Update – September 8, 2025

Covering Equities, Forex, Treasuries, Energy, Metals and Agriculture

“Markets are never obvious. The obvious trade is usually wrong.”

Honma Munehisa, The Fountain of Gold: The Three Monkey Record of Money (1755)

Honma Munehisa was an 18th-century rice trader in Japan, credited with inventing candlestick charting and recording one of the earliest studies of psychology in markets. There is a lot more to say about him, but let’s focus thus week on his lesson on the danger of the “obvious trade”, which is just as relevant centuries later.

So, what is the obvious trade today? Long the stocks, specifically S&P 500 and Nasdaq. It has been for a while, I like to call it “The Big Long”, drawing the reference from the famous movie. With ever-rising government debt and the erosion of money’s value, it seems like the only way to protect yourself. But is it? Many thought the same in the 1970s. Money supply grew rapidly, inflation was rampant, and stocks looked like the safe bet. Yet it took more than a decade for valuations to start making sense again. Meanwhile, the market went nowhere. By the end, investors were so frustrated that participation as a share of the population was the lowest since the Great Depression. At least at that time Gold and Silver did exceptionally well, just like we see today.

My base case is that we are facing a similar stretch of underperformance over the next five to ten years. Still, optimism dies hard. We may well push higher first. Passive-fueled dynamics are very strong. That is why I watch the trends carefully and act based on the combination of technicals, fundamentals, and crowd positioning, not on what seems obvious. The real opportunities may come not from the broad indices, but from thematic and sector-specific investments, where structural shifts, policy, and innovation can still drive significant returns.

That sets the tone for this week. This is update number fifty-one covering equities, forex, treasuries, metals, energy, and agricultural commodities, as always with a refreshed summary table and commentary across each market.

Kacper Piotr Kaminski – Cerlogic Markets Research, cerlogic.substack.com

This publication is for informational and educational purposes only and does not constitute investment advice. Markets involve risk, and every participant is responsible for their own decisions.

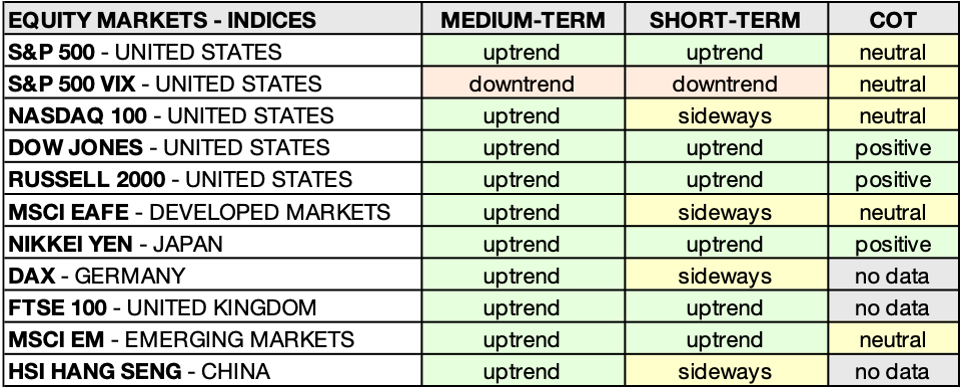

EQUITY MARKETS – INDICES

$SPX / $SPY, $NDX / $QQQ, $RUT / $IWM, $DAX, $FTSE, $NKD, $HSI, $KWEB

SHORT-TERM TREND CHANGES LAST WEEK:

· NIKKEI – JAPAN: Sideways 🟨 ➝ Uptrend 🟩

· MSCI EM – EMERGING MARKETS: Sideways 🟨 ➝ Uptrend 🟩

Selling pressure hit the NASDAQ $NDX / $QQQ early in the week, but buyers stepped in exactly at support. That level has held, but we are watching it closely. If support fails, we will look to short the index. Positioning remains stretched with asset managers heavily long and with extreme short exposure in $VIX.

The RUSSELL $RUT / $IWM squeeze we traded has run its course. We closed the position as risk–reward diminished, though the move could still extend. Now we can also see the DOW JONES benefit from flows rotating away from concentrated mega-cap tech exposure.

In Europe, both Germany and France have stalled under tariffs and a stronger euro. Southern markets such as Spain, Italy, and Greece remain more resilient. The UK’s FTSE 100 $FTSE is steady but still exposed to debt shocks and inflation risks.

In Asia, the NIKKEI $NKD is holding firm, supported by constant Bank of Japan liquidity and low energy prices. China’s HANG SENG $HSI remains stable but policy-driven. We continue to hold a small, tactical long in Chinese technology through $KWEB. The setup is constructive, but a clean breakout is still needed before the next leg higher, and even the strong move in $BABA was not enough to confirm. In fact, the MSCI EM index has returned to uptrend, with Brazil finally attracting fresh bids after weeks of lagging.

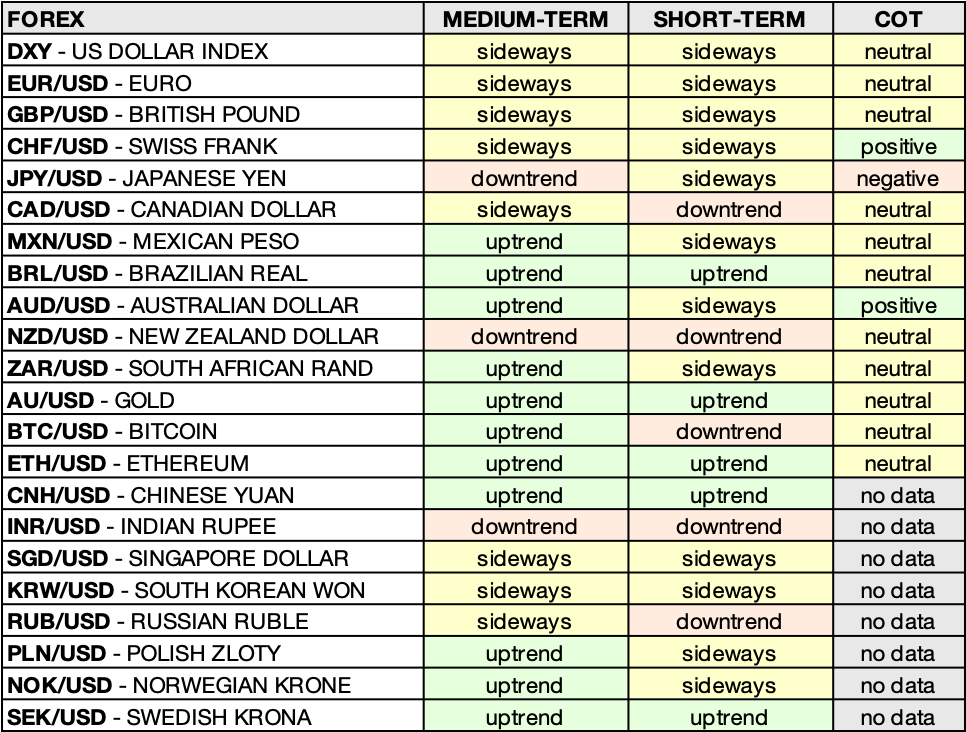

FOREX

$USD, $DXY, $EUR, $AU – GOLD, $CAD, $GBP, $CHF, $BTC

SHORT-TERM TREND CHANGES LAST WEEK:

· SEK/USD – SWEDISH KRONA: Sideways 🟨 ➝ Uptrend 🟩

The dollar $USD was hit on Friday after weak jobs data; immigration effects distorted the picture but it’s really getting difficult out there. The headline weakness flushed out most of the remaining longs. Even so, $DXY held key support. That level remains critical: a sustained close below 97.6 would open the path to 95, but as long as support holds, the trade to watch is the bounce. First resistance is at 99.0. A break and weekly close above that level would confirm a more durable uptrend with targets near 100.0 and 102.0.

Gold $AU is in clear breakout mode. We have been long since the 2024 structural uptrend, but we also take tactical positions, like the most recent long into the $3,450 breakout. That level has now given way, and the market is setting up for a push toward $3,800. A retest of $3,450 cannot be ruled out, but as long as it holds, the path is higher. Gold remains our core long with room to add tactically on pullbacks or fresh breakouts.

The Swiss franc $CHF is still the strongest currency in the world, yet asset managers continue to short it to fund risk. We are watching for the right moment to go long via options, but that would require risk assets to shift into downtrend and a liquidity squeeze to take hold.

Sterling $GBP remains on the short list for potential fundamental shorts, but the technicals are not lined up yet. The Canadian dollar $CAD stays heavy, with weak oil and tariffs weighing. Another weaker currency is New Zealand Dollar $NZD, no doubt low agricultural prices offer no help. Australian Dollar $AUD is in a much better position, I’d expect it lifted from a multi-year low in the next commodity bull market.

Bitcoin $BTC remains in short-term downtrend. To stabilize, it must recover $112K. Below that, the next supports are $106K and $100K, which would mark the first sustained downtrend in a long time.

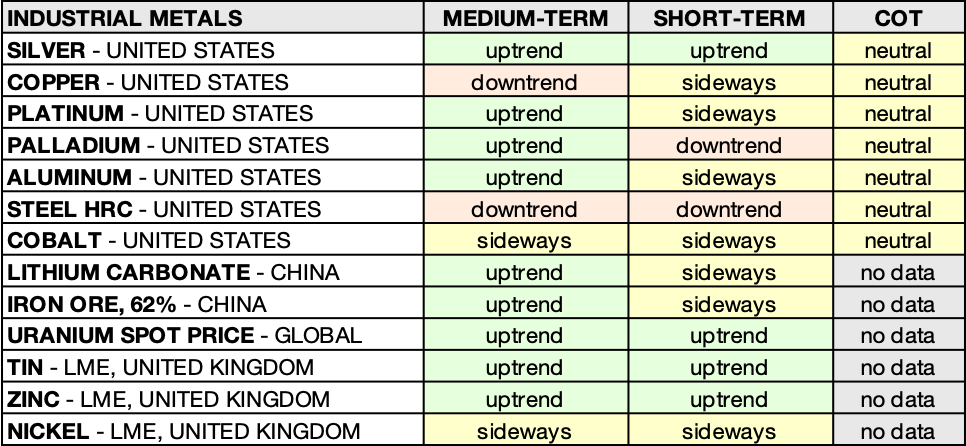

INDUSTRIAL METALS

$SLV, $PL / $PPLT, $PA / $PALL, $HG

SHORT-TERM TREND CHANGES LAST WEEK:

· LITHIUM CARBONATE – CHINA: Uptrend 🟩 ➝ Sideways 🟨

· IRON ORE, 62% – CHINA: Uptrend 🟩 ➝ Sideways 🟨

· TIN – LME, UNITED KINGDOM: Sideways 🟨 ➝ Uptrend 🟩

· ZINC – LME, UNITED KINGDOM: Sideways 🟨 ➝ Uptrend 🟩

Silver has broken out and confirmed the upside we had been watching for. We traded the breakout and already closed part of that position. If we reach $50, the remainder of the tactical long will also be exited, while the core position remains intact.

Platinum continues to consolidate above $1,290 after its earlier vertical move. We are still long from April, with $1,290 now serving as the risk and exit level for that position. Palladium remains weaker, still trading below $1,260 and tested now $1,100 before bouncing.

Copper has slipped back into downtrend. The tariff-driven distortions that temporarily lifted U.S. prices over the global market have now reversed, leaving producers again selling into weakness.

Lithium has cooled to sideways after its rebound from peak pessimism. Pullbacks are likely and should provide opportunities to build positions over time as demand may exceed current projections.

Uranium remains firm in uptrend across both time horizons. We continue to hold long positions, awaiting a potential repricing as the contracting cycle and seasonal demand into year-end gather momentum.

Iron ore has softened back to sideways after Chinese infrastructure support gave it a temporary lift. Tin and zinc have moved into uptrends on supply tightness, while nickel has stabilized, moving from downtrend to sideways after testing long-term lows.

ENERGIES

$CL, $NG, $XLE, $COAL

SHORT-TERM TREND CHANGES LAST WEEK:

· COAL – NEWCASTLE, AUSTRALIA: Sideways 🟨 ➝ Downtrend 🟥

Crude oil remains in short-term downtrend. Managed money has mostly abandoned the trade, leaving the market without a strong bid. Supply is adequate and demand uneven, keeping prices subdued for now.

Structurally, however, years of underinvestment and the likelihood of tighter producer discipline argue for much higher prices in the future. For us, this is not a short-term trading setup but the foundation of a long-term cycle. We are positioning through investing in oil and gas equities, building exposure to companies that can compound into the next upturn, but this may take a few years and we don’t treat it as trading.

Natural gas sits in the same spot. Speculative interest is light, and price momentum is lacking despite a clear path to long-term demand growth through exports to Asia and Europe.

Coal at Newcastle has now shifted to downtrend. Margins are squeezed at these levels, and production cuts are underway. Coal remains one of the most cyclical commodities, often providing deep-value opportunities when sentiment turns extremely negative. For now, though, the pressure is still to the downside.

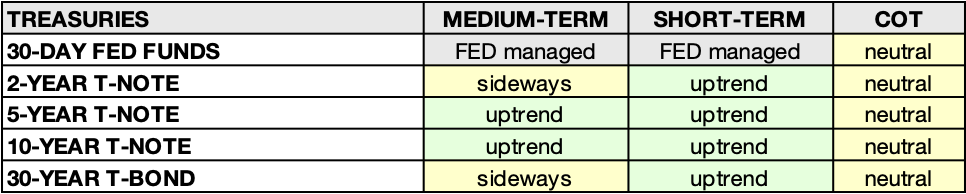

TREASURIES

$SHY, $IEF, $TLT

SHORT-TERM TREND CHANGES LAST WEEK:

· 30-YEAR T-BOND: Sideways 🟨 ➝ Uptrend 🟩

Treasuries remain highly sensitive to policy and data. Last week’s jobs report rattled the dollar and send bonds higher as well. Yields drifted lower, helping push the 5-year and 10-year into medium-term uptrends, while the 30-year also broke into short-term uptrend.

For now, we have no active trades in Treasuries. Our insurance position in $TUA (bet on lower 2-year yields) remains in place, if the Fed is politically overrun or we enter a recession and are forced into front-end cuts, that position should work. The risk lies in the long end, which last year sold off aggressively after cuts, and that scenario cannot be ruled out again.

Volatility has continued to come down since the tariffs-driven shock in April, but the policy backdrop keeps Treasuries difficult to own outright. Fiscal dominance remains the theme and attempts to control the curve at the long end make duration unattractive. In this environment, we prefer to stay patient and preserve optionality.

Near term, auctions and inflation prints will guide moves. Medium term, the bigger swing factors remain energy prices, trade policy, and banking regulation. A meaningful expansion of credit is still lacking, which limits inflation’s staying power beyond policy shocks.

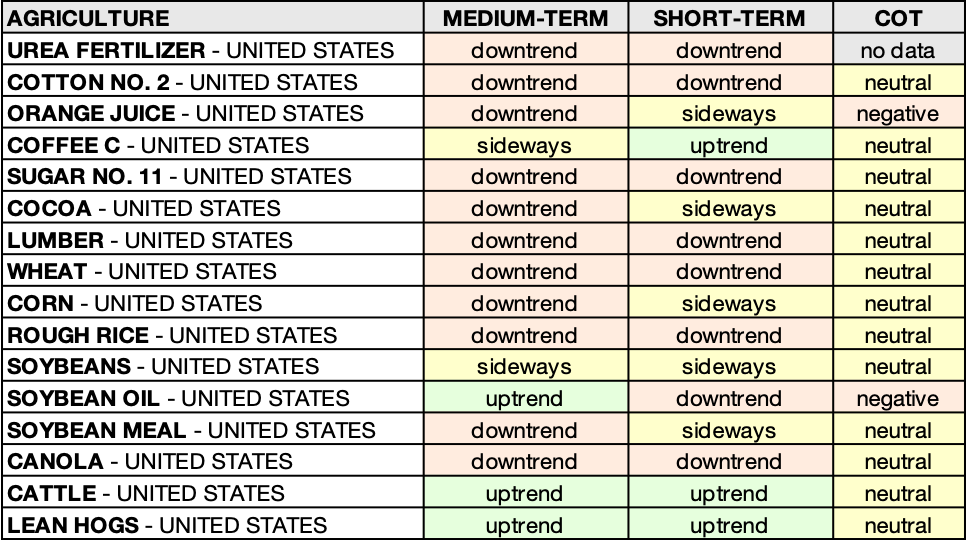

AGRICULTURE

$OJ, $KC, $CC, $LE, $GF, $ZL

SHORT-TERM TREND CHANGES LAST WEEK:

· UREA FERTILIZER – UNITED STATES: Sideways 🟨 ➝ Downtrend 🟥

· COTTON NO. 2 – UNITED STATES: Sideways 🟨 ➝ Downtrend 🟥

· ORANGE JUICE – UNITED STATES: Downtrend 🟥 ➝ Sideways 🟨

· SUGAR NO. 11 – UNITED STATES: Sideways 🟨 ➝ Downtrend 🟥

· SOYBEANS – UNITED STATES: Uptrend 🟩 ➝ Sideways 🟨

Agriculture remains one of the most policy-distorted markets. Tariffs, subsidies, and last-minute exemptions continue to dictate price action more than fundamentals. That has left many contracts chopping around, with multiple products sliding back into downtrend.

Soybeans, after showing promise, have slipped back into sideways. The broader oilseeds complex is mixed: Soybean Oil has lost momentum, Soybean Meal recovered modestly, while Canola is under renewed pressure. This divergence reinforces the point that policy and flows, not fundamentals, are driving price in the near term.

U.S. fertilizer prices are also rolling over, with Urea breaking into downtrend. While still expensive compared to pre-2020 levels, the short-term pullback eases cost pressure for farmers and could delay the next upward cycle in food inflation.

Among softs, Coffee is holding better, but Cotton and Cocoa have both turned lower, with weakness reflecting both higher supply and softer demand. Orange Juice has stabilized after recent volatility, but the market remains headline-driven, with tariff exemptions creating sharp reversals.

Protein remains the relative strength story. Cattle continues to trade strong as tariffs squeeze an already tight supply picture, while Hogs have also joined uptrend despite ample domestic supply.

That’s it for now. As always, reach out if you want to dig into anything further. Below you can find the key economic events this week and important earnings this week I may look at.

Stay safe out there!

Kacper Piotr Kaminski, Cerlogic Markets Research

Key Economic Events This Week

Times in GMT -5 / New York Time:

Tuesday, September 9

· 19:50 JPY: GDP (QoQ) (Q2)

Wednesday, September 10

· 08:30 USD: PPI (MoM) (Aug)

· 10:30 USD: Crude Oil Inventories

· 13:00 USD: 10-Year Note Auction

Thursday, September 11

· 08:15 EUR: Deposit Facility Rate (Sep)

· 08:15 EUR: ECB Interest Rate Decision (Sep)

· 08:30 USD: Core CPI (MoM) (Aug)

· 08:30 USD: CPI (YoY) (Aug)

· 08:30 USD: CPI (MoM) (Aug)

· 08:30 USD: Initial Jobless Claims

· 08:45 EUR: ECB Press Conference

· 13:00 USD: 30-Year Bond Auction

Friday, September 12

· 02:00 GBP: GDP (MoM) (Jul)

· 02:00 EUR: German CPI (MoM) (Aug)

Earnings this week I may look at:

Monday, September 8

· Casey’s General Stores $CASY US – Consumer Staples / Retail

· Restoration Hardware $RH US – Consumer Discretionary / Retail

· National Beverage $FIZZ US – Consumer Staples / Beverages

Tuesday, September 9

· Oracle $ORCL US – Technology / Software

· Synopsys $SNPS US – Technology / Software

· AeroVironment $AVAV US – Industrials / Defense

· GameStop $GME US – Consumer Discretionary / Retail

Wednesday, September 10

· Oxford Industries $OXM US – Consumer Discretionary / Apparel

Thursday, September 11

· Adobe Systems $ADBE US – Technology / Software

· Kroger $KR US – Consumer Staples / Retail

Great as every week. Let's hope that a stronger dollar won't stop gold and silver trend.

I was wondering if you don't do spread trading in commodities.

Thanks from Spain!