Weekly Markets Update – September 15, 2025

Covering Equities, Forex, Treasuries, Energy, Metals and Agriculture

“Victorious warriors win first and then go to war, while defeated warriors go to war first and then seek to win.”

Sun Tzu, The Art of War (5th century BC)

As far as we know, Sun Tzu never traded anything in his life, but I’d bet if he lived today, he would understand the markets better than most. His line about winning before the fight is really about preparation. Markets are not war, and war is not trading - but both are systems, and both are forms of art. And so, in both, the difference lies between those already in the right place when the move comes and those who rush in late, are chasing, or just hoping to get lucky. History shows the former collect the spoils while the latter become vanquished, they simply become liquidity.

It's important to accept that we operate in a world of probabilities, and be ready for every scenario, cause sooner or later it will come to pass. I never trust people who speak in certainties about markets. At best, I treat them as entertainment. Many analysts or money managers are very entrenched in their views about the dollar, about equities, bonds, about commodities, or any other of their favorite asset. They will typically not rest until you adapt their position. That sets all type of alarms in my mind. It is perhaps the most pronounced lately in equities, they certainly carry that whiff of inevitability, the passive tide pushing everything higher, or nothing stops this train rhetoric. I am not buying that, history teaches that tides can and do turn, and when they do, they surprise most and punish the unprepared.

So, the real question is: are you prepared for every scenario? Do you have a plan and know what to do when things go against you? If you do, yes, you may lose a few trades, a few battles, but you’ve already won the war, which is longer and requires commitment. Those who enter the field with only hope and ignorance, without preparation, have already lost, even if they get lucky now and then. That is the difference between strategy and gambling.

That sets the tone for this week, hopefully not too strong, but needed to be said. This is update number fifty-two, covering equities, forex, treasuries, metals, energy, and agricultural commodities, as always with a refreshed summary table and commentary across each market, see the bottom of the article.

Kacper Piotr Kaminski, Cerlogic Markets Research - cerlogic.substack.com

This publication is for informational and educational purposes only and does not constitute investment advice. Markets involve risk, and every participant is responsible for their own decisions.

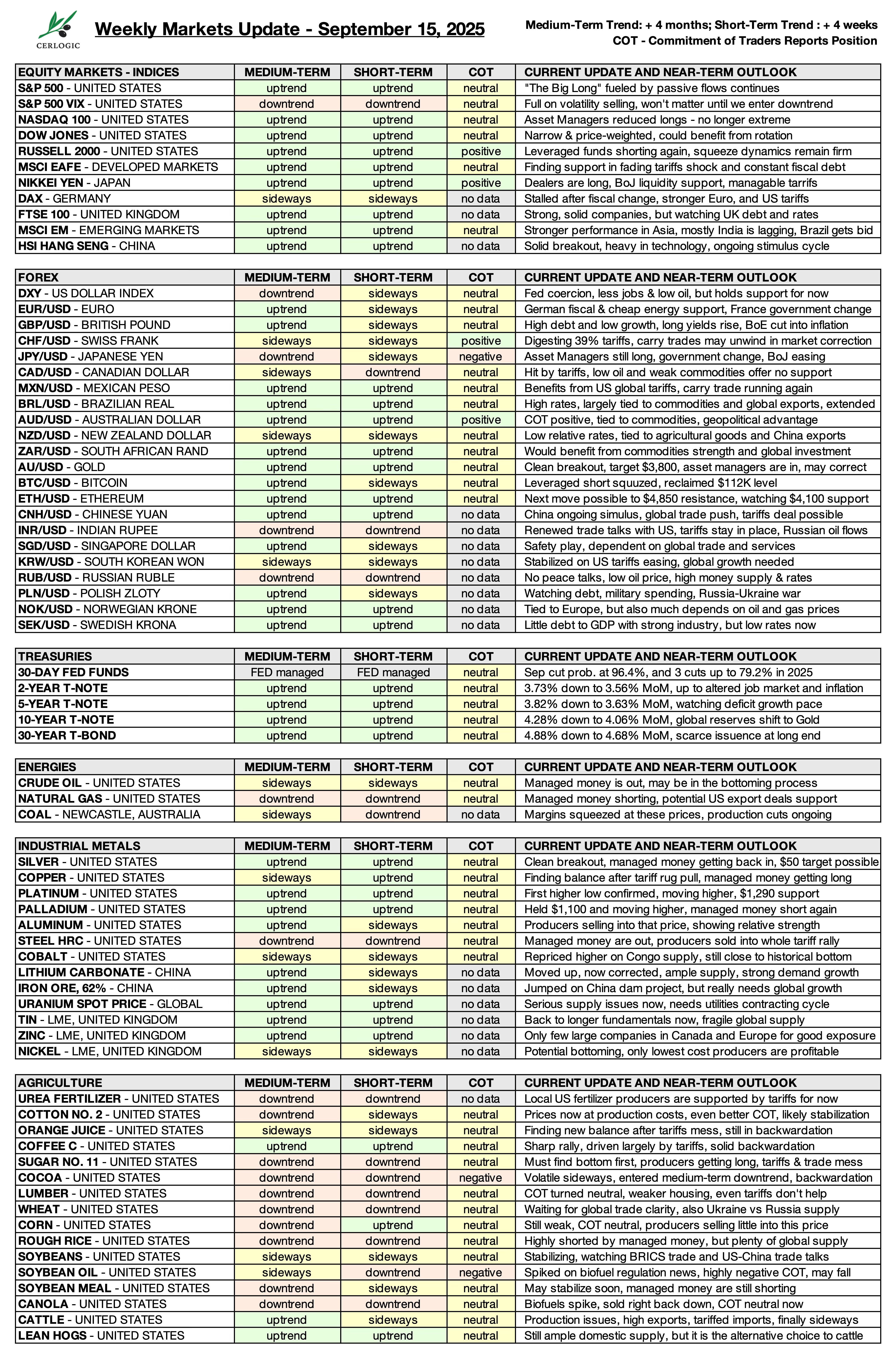

EQUITY MARKETS – INDICES

$SPX / $SPY, $NDX / $QQQ, $RUT / $IWM, $DAX, $FTSE, $NKD, $HSI, $KWEB

SHORT-TERM TREND CHANGES LAST WEEK:

· NASDAQ 100 – UNITED STATES: Sideways 🟨 ➝ Uptrend 🟩

· MSCI EAFE – DEVELOPED MARKETS: Sideways 🟨 ➝ Uptrend 🟩

· HSI HANG SENG – CHINA: Sideways 🟨 ➝ Uptrend 🟩

The S&P 500 $SPY is still in “The Big Long” dynamic. Passive flows dominate and volatility selling remains extreme. Until that cycle breaks the market keeps grinding higher. The NASDAQ $QQQ has bounced back into short term uptrend. It is worth noting that asset managers actually reduced their long exposure before the recent push higher. The Dow is also getting bid, and that is happening without any real rotation from mega caps. If rotation finally comes the Dow is the index quite likely to benefit. The Russell small caps $IWM still carry their squeeze potential. Leveraged funds are leaning short again and that is fuel for another rally.

In developed markets the MSCI EAFE moved back into uptrend. The Nikkei and the FTSE are doing the heavy lifting, supported by constant liquidity and fiscal expansion. The DAX in contrast stalled out. It slipped into sideways price action under pressure from a strong euro and weak industrial demand. France is showing the same pattern, while Spain, Italy and Greece are still pushing higher.

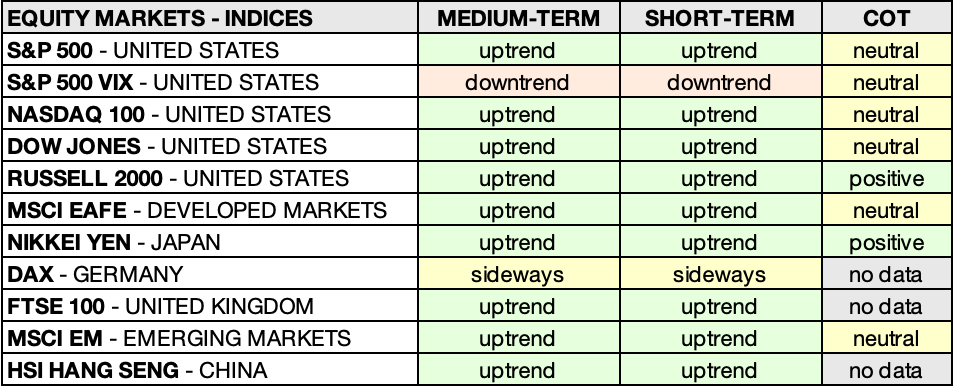

China’s Hang Seng $HSI / $KWEB has finally delivered a breakout. Stimulus and tech exposure carried it through, and for now the move looks like the real thing rather than another false dawn. As a consequence broader emerging markets, or growth markets which is a much better term, also moved into uptrend. India $INDA is still lagging under tariff pressure, but Brazil $EWZ is moving higher despite even higher ones. South Korea $EWY cannot be ignored either, as it remains one of the best performing markets year to date.

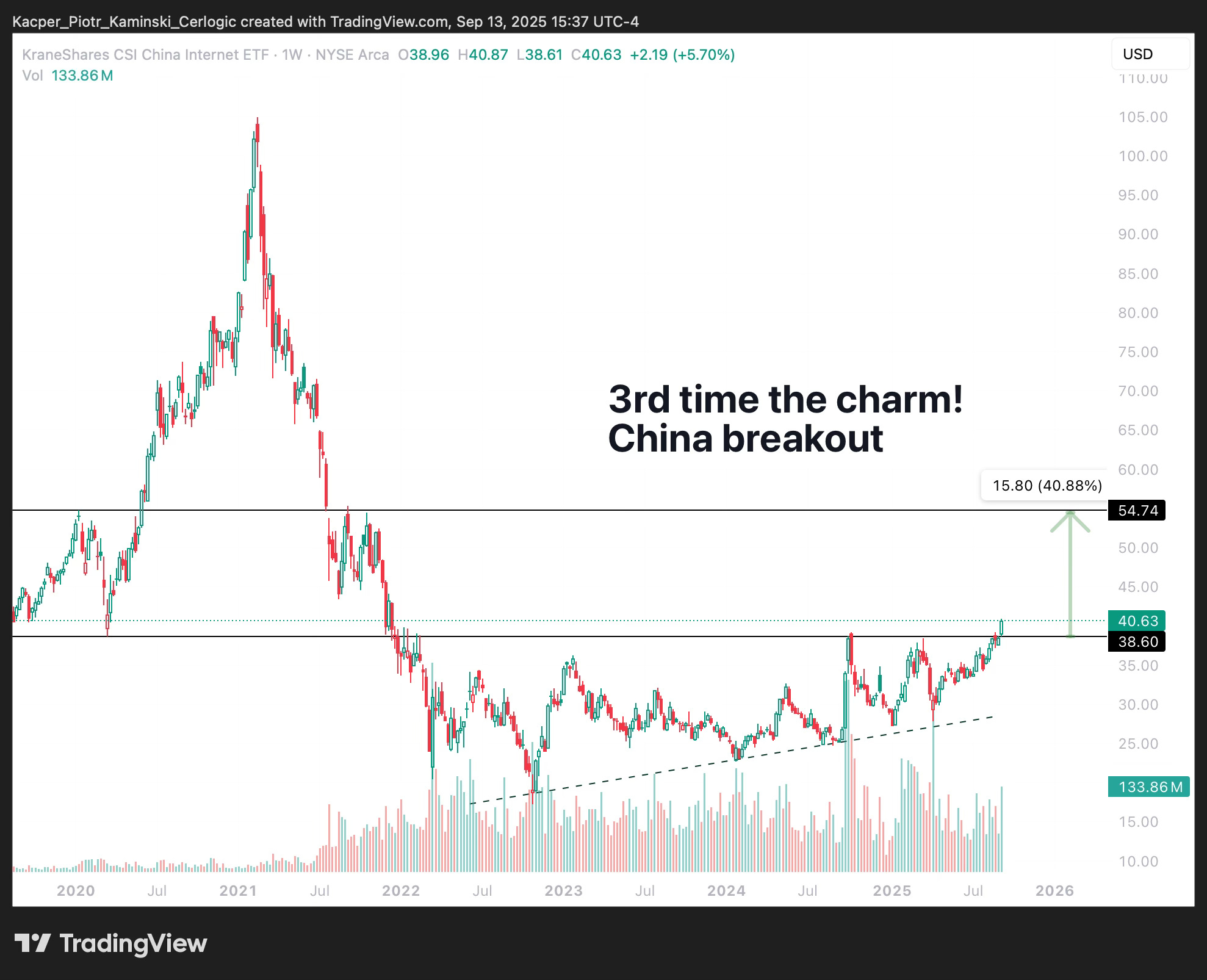

FOREX

$USD, $DXY, $EUR, $AU – GOLD, $CAD, $GBP, $CHF, $BTC

SHORT-TERM TREND CHANGES LAST WEEK:

· AUD/USD – AUSTRALIAN DOLLAR: Sideways 🟨 ➝ Uptrend 🟩

· NOK/USD – NORWEGIAN KRONE: Sideways 🟨 ➝ Uptrend 🟩

· ZAR/USD – SOUTH AFRICAN RAND: Sideways 🟨 ➝ Uptrend 🟩

· MXN/USD – MEXICAN PESO: Sideways 🟨 ➝ Uptrend 🟩

· BTC/USD – BITCOIN: Downtrend 🟥 ➝ Sideways 🟨

Another week of terrible news for the dollar $USD, but $DXY support still held. That level remains absolutely critical. A sustained close below 97.6 would open the path to 95, but as long as it holds the trade to watch is the bounce. Resistance sits at 99.0, and a weekly close above would confirm a more durable uptrend with targets near 100.0 and 102.0. For now the bears are frustrated, the longs are nervous, and the dollar keeps clinging to its line in the sand.

Gold $AU remains in clear breakout mode. We have been long since the 2024 structural uptrend and continue to trade it tactically. The $3,450 breakout level has held, and the market is setting up for a push toward $3,800. A retest of $3,450 cannot be ruled out, but as long as it holds the path is higher. Gold remains our core long with room to add tactically on pullbacks or fresh breakouts.

The Swiss franc $CHF is still the strongest currency in the world, yet asset managers continue to short it to fund risky trades. We are waiting for the right moment to go long via options, but that requires risk assets to flip into downtrend and a liquidity squeeze to commence.

The Japanese yen $JPY remains the weakest of the majors. The Bank of Japan still runs aggressive liquidity program, and the yen is still the preferred funding currency for carry trades. Every attempt at recovery is met with renewed selling pressure. Until policy shifts, the yen stays pinned, and that keeps pressure off the global risk assets.

Sterling $GBP has improved technically, though fundamentally it remains on the short list. The Canadian dollar $CAD continues to look heavy, pressured by weak oil and tariffs. The Australian dollar $AUD has finally picked up short term momentum and should be well positioned once the next commodity bull market takes hold. The New Zealand dollar $NZD managed to crawl out of downtrend into sideways, but high money supply, low rates and low agricultural prices could keep it pinned for now.

Bitcoin $BTC has stabilized back into sideways action. That is a small victory after its earlier downtrend, and a clean recovery would set the stage for a retest of the all-time highs. The potential is there, but the burden of proof lies with the bulls. To truly stabilize it must hold $112K. Below that level, the risks remain toward $106K and $100K, which would mark the first sustained downtrend in a long time.

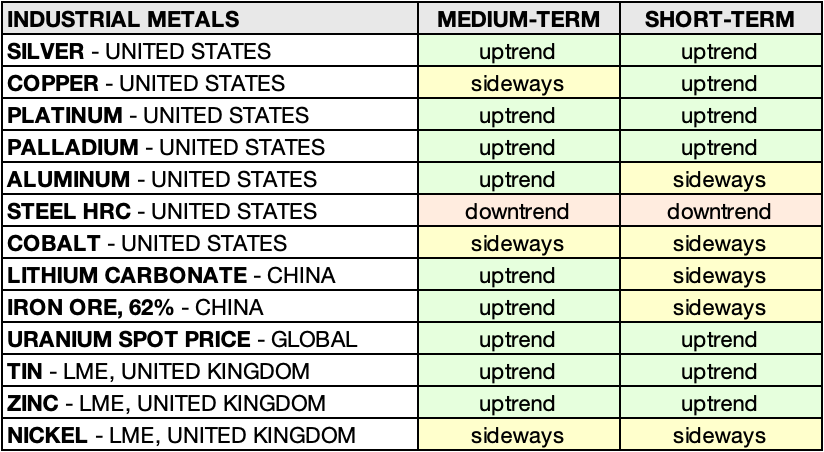

INDUSTRIAL METALS

$SLV, $PL / $PPLT, $PA / $PALL, $HG

SHORT-TERM TREND CHANGES LAST WEEK:

· PLATINUM – UNITED STATES: Sideways 🟨 ➝ Uptrend 🟩

· PALLADIUM – UNITED STATES: Downtrend 🟥 ➝ Uptrend 🟩

· COPPER – UNITED STATES: Sideways 🟨 ➝ Uptrend 🟩

Silver $SLV has held its breakout and continues to confirm the upside we had been watching for. We already booked partial profits, and the remainder of the tactical long will be exited if we reach $50. The core position remains intact and will remain so until this bull market is done.

Platinum $PL has regained short term momentum, moving back into uptrend. We are still long from April, with $1,290 as the risk and exit level. The consolidation phase may be ending, and the next leg higher is setting up. Palladium $PA also bounced, recovering into uptrend after testing lows near $1,100. For now, it looks more like a relief move than a structural reversal, but the pressure has eased.

Copper $HG is no longer in downtrend. It has recovered into sideways on the medium term and even pushed into short term uptrend. The distortions from tariffs that had temporarily lifted U.S. prices are gone, and producers are back selling into strength. Any sustained recovery still depends on broader industrial demand.

Lithium carbonate in China has cooled into sideways after its rebound from peak pessimism. Pullbacks should provide opportunities to build positions, as long term demand looks likely to exceed current projections.

Uranium continues to hold firm in uptrend across both medium and short-term horizons. We remain long and patient, awaiting a potential repricing as the contracting cycle and seasonal demand into year-end gather momentum.

Iron ore has softened back into sideways after Chinese infrastructure support gave it a temporary lift. Tin and zinc both remain in uptrend on supply tightness. Nickel has stabilized, moving from downtrend to sideways after testing long term lows.

ENERGIES

$CL, $NG, $XLE, $COAL

SHORT-TERM TREND CHANGES LAST WEEK:

· CRUDE OIL – UNITED STATES: Downtrend 🟥 ➝ Sideways 🟨

Crude oil $CL has steadied, moving from downtrend into sideways on the short-term horizon. Managed money remains absent, which leaves the market without a real bid, but at least the aggressive selling pressure has eased. There is also a chance that oil is building a higher low here, the beginning of a bottoming process. Supply remains adequate and demand patchy, keeping price action choppy.

Structurally, nothing has changed. Years of underinvestment and tighter discipline among producers still argue for much higher prices in the future. For us this is not a short-term trading setup but the foundation of the next cycle. We continue to position through oil and gas equities, building exposure to companies that can compound into the upturn. That will take patience, and we do not treat it as trading.

Natural gas $NG is still in the same position. Speculative flows are light, and price momentum is missing, even though the long-term demand story through exports to Asia and Europe remains likely in the future.

Coal $COAL at Newcastle has lost momentum, moved to downtrend in the short-term and also slipping from medium term uptrend into sideways price action. Margins are still being squeezed, and producers are cutting output. Coal remains one of the most cyclical markets, and it will offer deep value again when sentiment turns dark enough. For now, the pressure is neutral to lower.

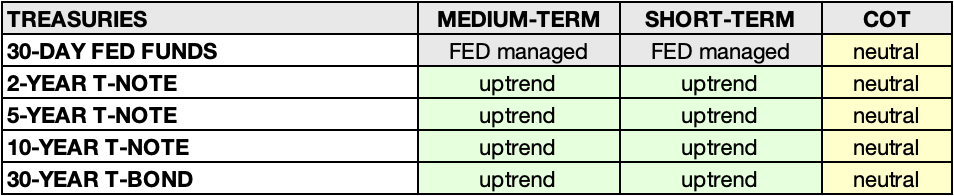

TREASURIES

$SHY, $IEF, $TLT

NO SHORT-TERM TREND CHANGES LAST WEEK

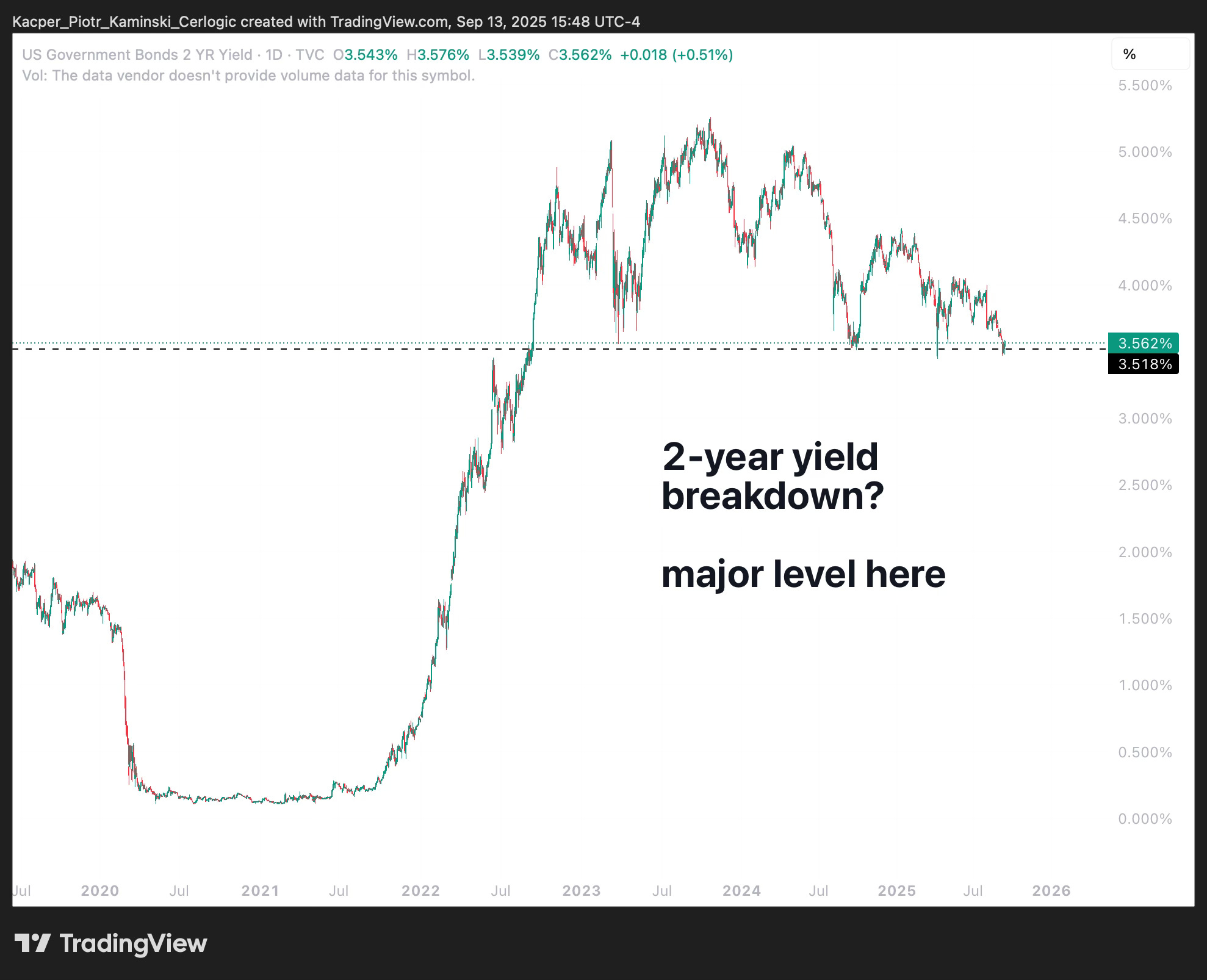

Treasuries remain highly sensitive to data, and the latest weaker job market numbers added fuel to the rally. The labor report looked soft at first glance, but much of the weakness comes from the immigration halt that is now distorting the statistics. Still, the market trades the headline, and yields moved lower across the curve. That was enough to push both the 2-year and the 30-year into medium term uptrend, while the long bond also picked up short term momentum.

We continue to hold our insurance position with a bet on lower 2-year yields. If the Fed is politically overrun or a recession forces front-end cuts, that position should work. The risk sits in the long end. Last year the 30-year sold off aggressively even after cuts, and that scenario cannot be ruled out again.

Volatility has eased since the tariff shock in April, but Treasuries remain difficult to own outright. Fiscal dominance is still the theme, and attempts to control the curve make duration unattractive. In this environment we prefer to stay patient and preserve optionality.

Near term, auctions and inflation prints will guide the moves. Medium term, the key swing factors are energy prices, trade policy, and banking regulation. Without a meaningful expansion of credit, inflation lacks staying power beyond the occasional policy shock.

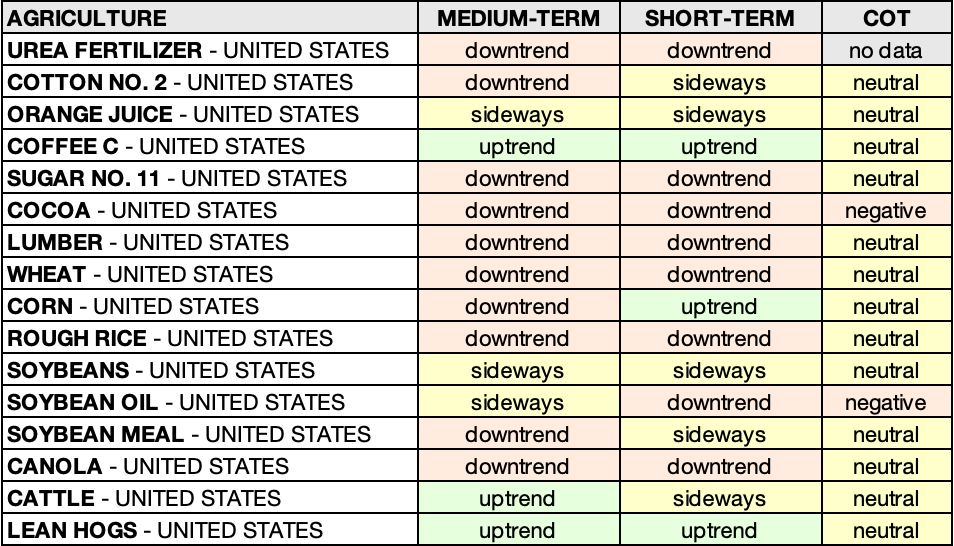

AGRICULTURE

$OJ, $KC, $CC, $LE, $GF, $ZL

SHORT-TERM TREND CHANGES LAST WEEK:

· CORN – UNITED STATES: Sideways 🟨 ➝ Uptrend 🟩

· COTTON NO. 2 – UNITED STATES: Downtrend 🟥 ➝ Sideways 🟨

· COCOA – UNITED STATES: Sideways 🟨 ➝ Downtrend 🟥

· CATTLE – UNITED STATES: Uptrend 🟩 ➝ Sideways 🟨

Among softs, Coffee $KC remains the standout. It has broken into full uptrend, driven largely by tariffs and trade flows. The market is in steep backwardation, but interestingly producers are not selling into the rally in size, which keeps the squeeze alive. Cocoa $CC has slipped back into downtrend, price action looks heavy and producers remain short, it may just move lower. Cotton $CT stabilized into sideways, which is at least better than before, as prices have now fallen to production cost levels. Sugar $SB may be reaching a bottom, but it has to carve it out first before we can call it. Orange Juice $OJ continues to chop around, fully headline-driven.

The soybean complex is fragmented and politically sensitive. Soybeans $ZS remain in sideways, with traders watching BRICS trade flows and the possibility of a US-China deal. That deal keeps moving further away, and the lack of progress weighs on sentiment. Soybean Oil $ZL has fallen back into downtrend after the short-lived biofuel regulation spike, while Soybean Meal $ZM has stabilized into sideways from downtrend. Managed money remains short meal, but the worst of the liquidation may be behind it. Canola $RS remains weak and is still searching for a base.

Corn $ZC has pushed into short term uptrend, though producers started selling into it so COT positioning remains neutral. Wheat $ZW deserves attention here. It has been grinding lower for years and any rally of consequence will require fresh demand.

Fertilizer prices also remain under pressure for now. Urea turned firmly into downtrend, but the producer price is still climbing. That eases input costs for farmers, and delays the next inflationary cycle in food commodities.

Protein markets are no longer invincible. Cattle $LE slipped to sideways price action, but production issues, exports, and tariffed imports still remain in place. Hogs $HE remain in uptrend, acting as the substitute protein in tariff-distorted trade flows, even though domestic supply remains ample.

That’s it for now. As always, reach out if you want to dig into anything further. Below you can find the key economic events this week and important earnings this week I may look at.

Stay safe out there!

Kacper Piotr Kaminski, Cerlogic Markets Research - cerlogic.substack.com

Key Economic Events This Week

Times in GMT -5 / New York Time:

Monday, September 15

All Day: 🇯🇵 Holiday, Japan, Respect for the Aged Day

Tuesday, September 16

08:30 🇺🇸 USD: Core Retail Sales (MoM) (Aug)

08:30 🇺🇸 USD: Retail Sales (MoM) (Aug)

Wednesday, September 17

02:00 🇬🇧 GBP: CPI (YoY) (Aug)

05:00 🇪🇺 EUR: CPI (YoY) (Aug)

09:45 🇨🇦 CAD: BoC Interest Rate Decision

10:30 🇺🇸 USD: Crude Oil Inventories

14:00 🇺🇸 USD: FOMC Economic Projections

14:00 🇺🇸 USD: FOMC Statement

14:00 🇺🇸 USD: Fed Interest Rate Decision

14:30 🇺🇸 USD: FOMC Press Conference

Thursday, September 18

07:00 🇬🇧 GBP: BoE Interest Rate Decision (Sep)

08:30 🇺🇸 USD: Initial Jobless Claims

08:30 🇺🇸 USD: Philadelphia Fed Manufacturing Index (Sep)

23:00 🇯🇵 JPY: BoJ Interest Rate Decision

Earnings this week I may look at:

Tuesday, September 16

Ferguson $FERG LN – Industrials / Distribution

JTC $JTC LN – Financials / Services

Wednesday, September 17

General Mills $GIS US – Consumer Staples / Food

Barratt Redrow $BDEV LN – Consumer Discretionary / Homebuilders

KB Home $KBH US – Consumer Discretionary / Homebuilders

Cracker Barrel Old Country Store $CBRL US – Consumer Discretionary / Restaurants

Thursday, September 18

FedEx $FDX US – Industrials / Transportation

Lennar $LEN US – Consumer Discretionary / Homebuilders

Darden Restaurants $DRI US – Consumer Discretionary / Restaurants

NEXT $NXT LN – Consumer Discretionary / Retail

FactSet Research Systems $FDS US – Technology / Data & Analytics

Renishaw $RSW LN – Technology / Engineering