Weekly Markets Update – September 1, 2025

Free, always - Covering Equities, Forex, Treasuries, Energy, Metals and Agriculture

“If you can learn to create a state of mind that is not affected by the market’s behavior, the struggle will cease to exist. The consistency you seek is in your mind, not in the markets.” - Mark Douglas, author of the modern classic Trading in the Zone book (2000).

How many times have you thought that markets make no sense, that illogical things keep happening, and that price action refuses to match what you believe should be true? Most of us at some point has felt that frustration.

Douglas was a trader himself, but he is remembered above all as one of the great teachers of trading psychology. He argued that this consistency we naturally seek is never found in the market itself, but in the trader’s own state of mind, it comes from the ability to stick to a process without being thrown off by every swing of price action.

That insight feels as relevant today as ever. Markets will always tempt us to chase, panic into weakness, or fight moves that appear irrational. Price action will always swing, sometimes violently and without clear reason. What matters is the ability to stay consistent when the crowd bends in every direction. We can’t control where and when the markets will move, but we can control how we react to it.

That sets the tone for this week. This is update number fifty. Over the past year I have shared insights covering equities, forex, treasuries, metals, energy, and agricultural commodities, as always with a refreshed summary table and commentary across each market.

Kacper Piotr Kaminski – Cerlogic Markets Research

This publication is for informational and educational purposes only and does not constitute investment advice. Markets involve risk, and every participant is responsible for their own decisions.

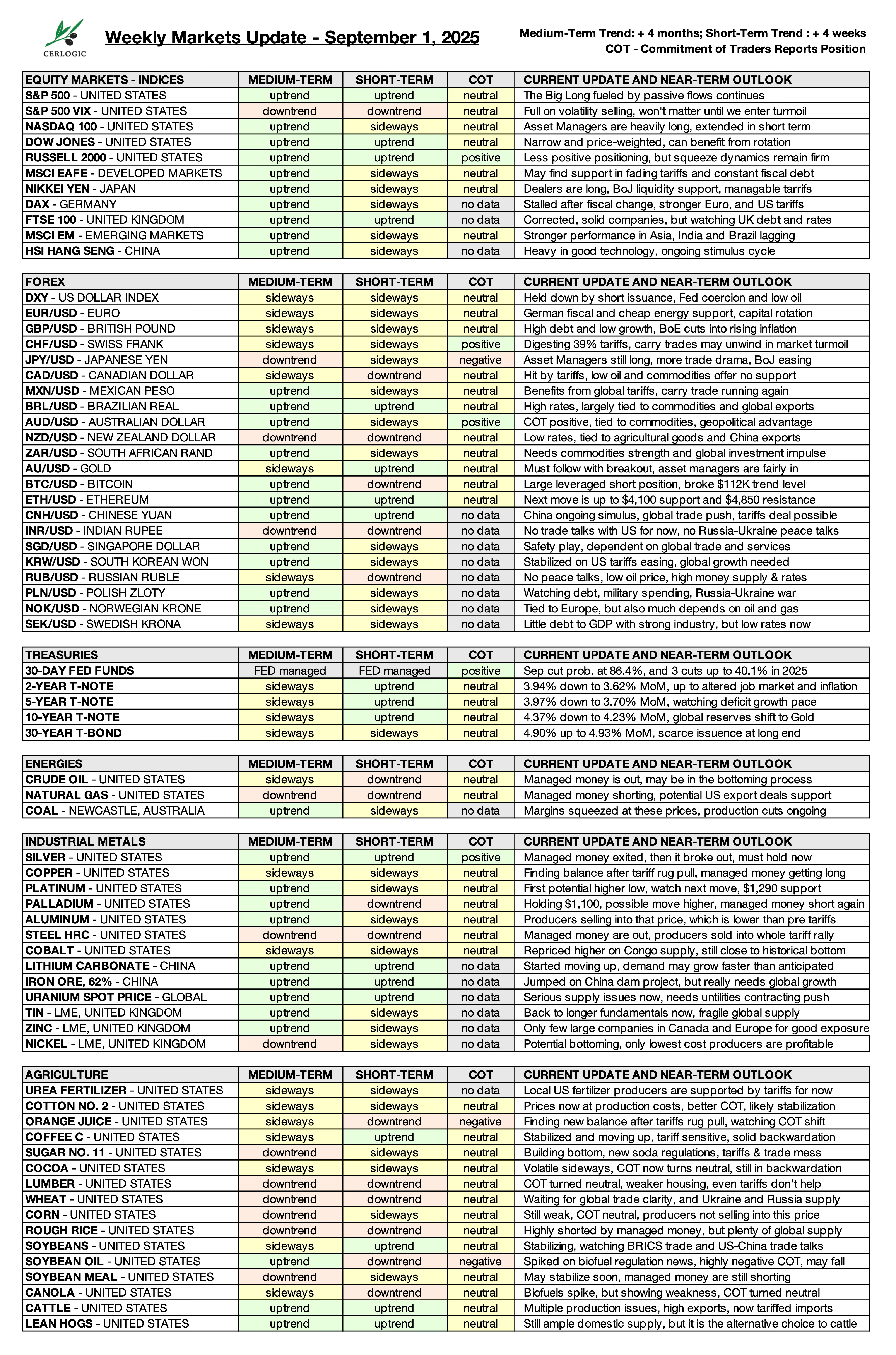

EQUITY MARKETS – INDICES

$SPX / $SPY, $NDX / $QQQ, $RUT / $IWM, $DAX, $FTSE, $NKD, $HSI, $KWEB

SHORT-TERM TREND CHANGES LAST WEEK:

· MSCI EAFE – DEVELOPED MARKETS: Uptrend 🟩 ➝ Sideways 🟨

· NIKKEI – JAPAN: Uptrend 🟩 ➝ Sideways 🟨

· MSCI EM – EMERGING MARKETS: Uptrend 🟩 ➝ Sideways 🟨

· HSI HANG SENG – CHINA: Uptrend 🟩 ➝ Sideways 🟨

For months, positioning has been dominated largely by a single macro trade: long NASDAQ $NDX / $QQQ mega-cap technology, sell volatility to extremes, and short RUSSELL $RUT / $IWM small caps. That dynamic is now unwinding. The NASDAQ remains stuck in sideways price action with asset managers still heavily long. Even Powell’s dovish speech at Jackson Hole could not provide a breakout, which shows just how stretched is the positioning.

The RUSSELL, by contrast, staged a sharp squeeze last week. We caught that move on the long side, but with about two-thirds of the rally already behind us, we closed the position in line with our risk–reward parameters. The squeeze may extend further, but the asymmetry is fading. The DOW JONES also benefited from renewed rotation, attracting flows away from the narrow concentration in tech.

In Europe, momentum has cooled. The German DAX $DAX is weighed down by tariffs and a stronger euro, while southern markets such as Spain, Italy, and Greece remain more resilient, for now. The FTSE 100 $FTSE holds steady even after correction, but remains highly vulnerable to the risks of inflation, debt, and rising rates.

In Asia, both the NIKKEI $NKD and HANG SENG $HSI lost momentum, shifting to sideways. Japan still benefits from low energy costs and the Bank of Japan’s ongoing support, but near-term impulse has weakened. In China, we are trading lightly long in technology via $KWEB. A breakout is still needed for the next leg higher, and it has not yet materialized despite a monster move in $BABA last week.

It is still good to remember, global equities remain tied together. They may diverge short term, but when positioning unwinds, they usually move together, especially on the downside.

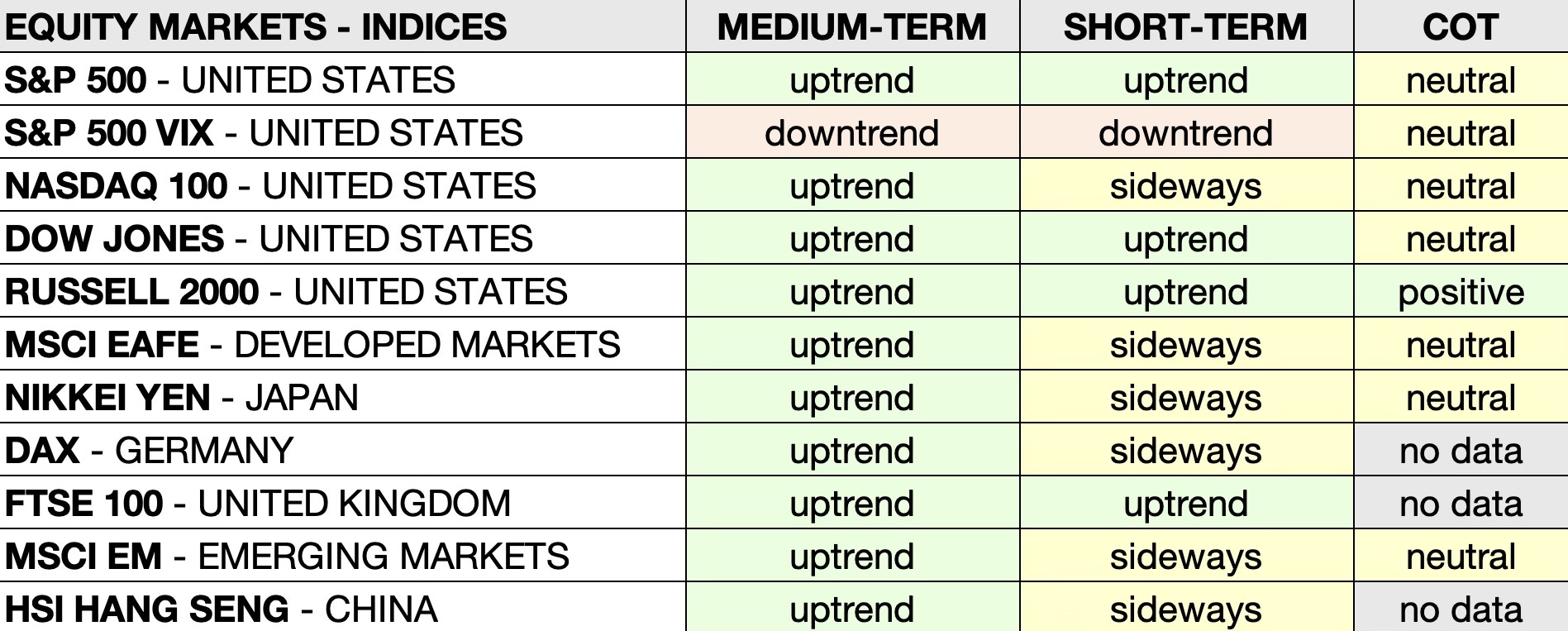

FOREX

$USD, $DXY, $AU – GOLD, $CAD, $GBP, $CHF, $BTC

SHORT-TERM TREND CHANGES LAST WEEK:

· BTC/USD – BITCOIN: Sideways 🟨 ➝ Downtrend 🟥

· CNH/USD – CHINESE YUAN: Sideways 🟨 ➝ Uptrend 🟩

The key question in the forex market remains the direction of the US dollar $USD. It rose steadily into Powell’s Jackson Hole speech two weeks ago, then bounced a little, only to retrace again on Trump’s attempt to fire Fed Governor Lisa Cook. It appears to have found a near-term bottom, but it is still unclear whether the longer-term downtrend will resume. Much depends on US politics, the Fed’s ability to act independently, and incoming economic data such as jobs numbers and inflation.

Technically, if the dollar index $DXY closes the week below 97.6, the next downside target would be 95.0. A close above 99.0, however, would likely trigger a more sustained uptrend. The dollar’s direction matters across almost all markets, particularly in commodities and emerging market equities.

For the dollar to regain lasting strength, it must also be allowed to. Now, the Fed Chair faces intense political pressure, including verbal attacks and even the threat of personal legal action. This could force faster or deeper rate cuts, even as inflation rises again, which would undermine the dollar. One supportive factor is the Treasury’s ongoing effort to refill the TGA account, which drains liquidity from the system. But that impact has been largely offset by a decision to concentrate issuance at the short end.

Meanwhile, it has been a few months since gold paused its parabolic rise for a much-needed consolidation. The spot price is once again attempting a breakout above $3,450. It must rise a little higher and hold that level for the next leg up.

What else is new, oh yes, asset managers are once again shorting the strongest currency in the world, the Swiss franc $CHF, using it as a funding vehicle to engage in riskier activities. Meanwhile, the Canadian dollar $CAD is under pressure, hit by both lower oil prices and sticky US tariffs, particularly painful given the co-dependence of the two economies. Personally, I’m also hunting for the British pound $GBP short. I’d love it more with proper technicals lining up to what is a great fundamental case. Finally, there is Bitcoin $BTC. Momentum has shifted into a downtrend, and it must reclaim $112K to stabilize. On the downside, the next key support levels are $106K and $100K.

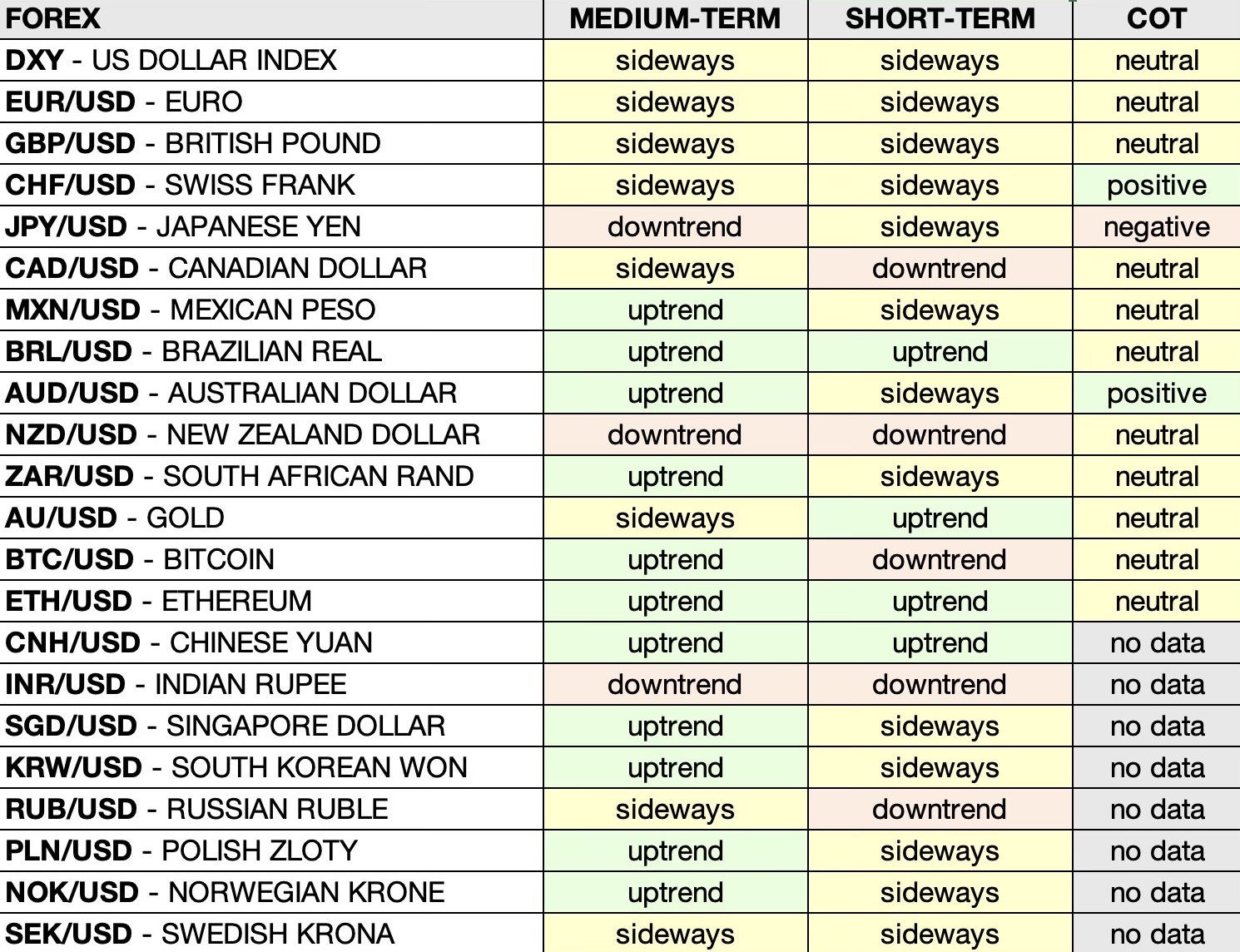

INDUSTRIAL METALS

$SLV, $PL / $PPLT, $PA / $PALL, $HG

SHORT-TERM TREND CHANGES LAST WEEK:

· SILVER – UNITED STATES: Short-term Sideways 🟨 ➝ Uptrend 🟩

· COPPER – UNITED STATES: Short-term Downtrend 🟥 ➝ Sideways 🟨

· PALLADIUM – UNITED STATES: Short-term Sideways 🟨 ➝ Downtrend 🟥

· IRON ORE, 62% – CHINA: Short-term Sideways 🟨 ➝ Uptrend 🟩

Let’s start with silver. The target at $38 was finally reached some time ago, followed by a push higher, a retracement, and now a clean breakout. The key technical levels remain the same: support at $35 and the all-time high near $50, which could start acting like a magnet. We were signaling for some time that positioning had cleared and the potential for upside was in place - that move has now materialized. The best companies continue to enjoy strong margins at these prices.

Platinum has retraced from its earlier vertical move, found support at $1,290, and is consolidating. Given the speed of the initial rally, it may take more time before the next meaningful leg develops. Palladium, meanwhile, has slipped into a short-term downtrend after breaking below $1,260 and is hovering near the longer-term technical level of $1,100.

Copper remains a story of policy distortions. The tariff-driven squeeze, particularly the fifty percent figure, punished producers and sent US prices to a 30% premium over the global market, hurting domestic industry broadly. That policy was quickly scrapped, leaving the new longs stranded. Now that prices are back in line with the global market, the focus can return to long-term fundamentals. Technically, copper has stabilized, moving from downtrend to sideways, which gives the market some breathing room.

Lithium is showing signs of life. The equities bounced from what looks like a capitulation bottom, just as we argued peak pessimism would offer opportunity. With supply still adequate, pullbacks are likely, giving multiple chances to build a position. Demand may well rise faster than consensus projections, so this is an area to keep on the radar.

Uranium has regained strength, with both medium- and short-term trends holding in uptrend. The earlier correction was largely technical, tied to speculative positioning around the Sprott Trust. Fundamentals remain intact, with the contracting cycle and seasonal demand expected to pick up into year end.

Iron ore has also strengthened, shifting into a short-term uptrend. The recent bounce reflects infrastructure and stimulus activity in China, but to sustain it, a broader global growth impulse will be required.

Other industrial metals such as tin, zinc, and nickel are still mostly moving sideways. A more coordinated global growth cycle will be needed before they can make substantial progress.

ENERGIES

$CL, $NG, $XLE, $COAL

Crude oil remains in a short-term downtrend, while managed money has largely exited the trade, leaving prices to drift without strong direction. Supply remains adequate, while demand signals are uneven, and that combination keeps crude range-bound for now. The longer-term picture is different. Years of underinvestment and the likelihood of tighter production discipline from major producers still argue for structurally higher prices over time, even if the near-term outlook is soft.

Natural gas is in a similar position. Despite potential growth in export demand, especially from Asia and Europe, speculative flows remain light and prices lack a sustained bid. Seasonal demand may help later in the year, but for now the market trades quietly.

Coal, specifically thermal coal at Newcastle, remains in a medium-term uptrend but has moved sideways short term. At current levels, producer margins are squeezed and production cuts are underway. Longer term, coal continues to behave cyclically, offering opportunities when sentiment turns deeply negative and prices approach depression levels.

TREASURIES

$SHY, $IEF, $TLT

I have no active trades in Treasuries and do not plan to add new ones until the dust settles. Tariffs need to remain in place long enough, or be scrapped entirely as it seems possible now, to give better visibility on jobs and growth. If the Fed is overrun by the President and front-end rates drop sharply, this position should perform very well. The reaction at the long end is less certain. Last year, when the Fed cut rates, yields spiked higher, and a similar outcome cannot be ruled out. Normally I would consider TIPS at current yields, but without an independent statistical office the United States lacks a credible measure of inflation, which makes such allocation difficult to justify.

Powell’s Jackson Hole speech was the main event last week. Markets perceived it as dovish, but it is important to note that rate cut probabilities did not move significantly. It was equities that responded most strongly, while Treasuries traded more in line with recent ranges.

Volatility has come down sharply since the April tariffs-driven crash, as shown by the MOVE index. The spending bill also removed a major source of uncertainty and reinforced that fiscal policy is now the dominant force in markets. Even so, I am not interested in holding bonds. There is a plausible path for yields to rise significantly over the rest of the decade. Market forces remain real, and government intervention to support the long end only makes duration less appealing. In this environment, there are better uses of capital or even safer places to simply hold liquidity.

Near to medium term, Treasuries will take their direction from energy markets, trade policy, and regulatory shifts. Tariffs affect growth and jobs directly, while banking regulation will shape credit creation. Without a meaningful expansion in credit, it is difficult to sustain inflation, and trade policy alone is not enough. Another factor worth monitoring is the stablecoin legislation, which is designed to channel demand into Treasuries. This adds to the bid for government paper but also raises important questions about how cross-border flows and global payments may evolve as the system matures.

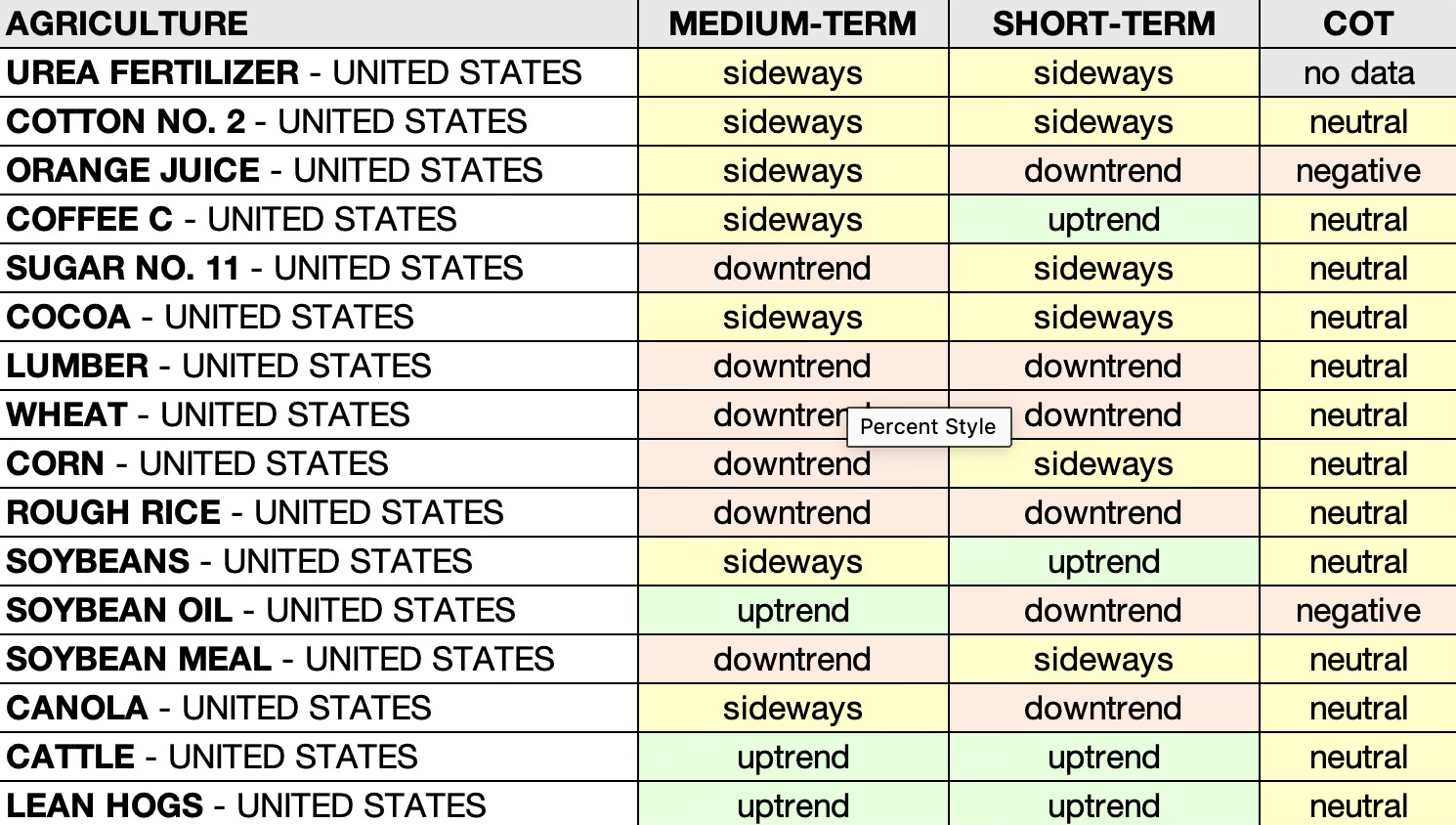

AGRICULTURE

$OJ, $KC, $CC, $LE, $GF, $ZL

SHORT-TERM TREND CHANGES LAST WEEK:

· UREA FERTILIZER – UNITED STATES: Medium-term Uptrend 🟩 ➝ Sideways 🟨

· LUMBER – UNITED STATES: Medium-term Sideways 🟨 ➝ Downtrend 🟥

· SOYBEAN OIL – UNITED STATES: Short-term Sideways 🟨 ➝ Downtrend 🟥

· SOYBEAN MEAL – UNITED STATES: Short-term Uptrend 🟩 ➝ Sideways 🟨

· LEAN HOGS – UNITED STATES: Short-term Sideways 🟨 ➝ Uptrend 🟩

Agriculture markets remain largely event-driven, with tariffs and policy shifts acting as the primary disruptors. Anything not produced domestically continues to enjoy some form of tariff support, which benefits soft commodities the most. Grains remain under pressure from surplus supply. With the new BBB bill and strong government support for farmers, there is little sign of supply destruction for now. Export deals are still elusive, and while some markets are reopening, the lasting impact will not be clear until conditions stabilize.

Soybean Oil, however, slipped into a short-term downtrend. The earlier biofuels-driven rally has lost momentum, with positioning turning less favorable and speculative flows pulling back. Soybean Meal has also cooled, reverting to sideways after a brief recovery. Together, these moves highlight how uneven momentum is across the complex.

Among softs, coffee remains firm, while cocoa is still moving violently sideways. Orange juice is still in a downtrend, unwinding the earlier tariff-driven spike. Lumber has weakened further despite tariffs, which is telling a lot about the housing and construction activity.

Protein markets are stronger. Cattle remains the leader, still in uptrend, while lean hogs moved into a short-term uptrend after trading sideways. For cattle specifically, tariffs are pushing prices higher at a time when supply is already tight. Expanding production requires both time and capital, which keeps constant upward pressure in place.

That’s it for now. As always, reach out if you want to dig into anything further. Below you can find the key economic events this week and important earnings this week I may look at.

Stay safe out there!

Kacper Piotr Kaminski, Cerlogic Markets Research

Key Economic Events This Week (Times in GMT -5 / New York Time):

Monday, September 1

United States – Labor Day (Holiday)

Canada – Labor Day (Holiday)

Tuesday, September 2

EUR: CPI (YoY) (Aug)

USD: S&P Global Manufacturing PMI (Aug)

USD: ISM Manufacturing PMI (Aug)

USD: ISM Manufacturing Prices (Aug)

Wednesday, September 3

USD: JOLTS Job Openings (Jul)

Thursday, September 4

USD: ADP Nonfarm Employment Change (Aug)

USD: Initial Jobless Claims

USD: S&P Global Services PMI (Aug)

USD: ISM Non-Manufacturing PMI (Aug)

USD: ISM Non-Manufacturing Prices (Aug)

USD: Crude Oil Inventories

Friday, September 5

USD: Average Hourly Earnings (MoM) (Aug)

USD: Nonfarm Payrolls (Aug)

USD: Unemployment Rate (Aug)

Earnings this week I might take a look at:

Tuesday, September 2

Zscaler (ZS:US) – Technology

NIO (NIO:US) – Automobiles

Wednesday, September 3

Salesforce (CRM:US) – Technology

Swiss Life Holding (SLHN:SW) – Financials / Insurance

Dollar Tree (DLTR:US) – Consumer Staples / Retail

Hewlett Packard Enterprise (HPE:US) – Technology

Macy’s (M:US) – Consumer Discretionary / Retail

American Eagle Outfitters (AEO:US) – Consumer Discretionary / Retail

Foot Locker (FL:US) – Consumer Discretionary / Retail

Thursday, September 4

Broadcom (AVGO:US) – Technology / Semiconductors

Copart (CPRT:US) – Industrials / Services

Lululemon Athletica (LULU:US) – Consumer Discretionary / Apparel

DocuSign (DOCU:US) – Technology / Software