Markets Update – September 22, 2025

Covering Equities, Forex, Treasuries, Energy, Metals and Agriculture

“Nobody ever lost money taking a profit.”

Bernard Baruch - one of the greatest traders of all time

Baruch’s line is one of the oldest reminders in markets, but it is worth repeating, particularly today. Markets are running hot, with strong uptrends across many asset classes. We are long and happy with the gains, and in our view, there is more to come, particularly in sectors that are not the flavor of the day. As for the darlings of the crowd, it is easy to fall for the illusion that every rally will keep running, or that the perfect exit lies just a little bit higher. That temptation is what Wall Street shorthand calls being a pig. The reality is that discipline, not greed, decides who keeps their capital and who hands it back.

We are not selling the core positions as long as the market is acting right. What we are doing is trimming, taking some money off the table, if only to have dry powder ready to deploy later. The purpose of trading is not to capture every last cent of a move, but to stay solvent and consistent across many moves to come. Those who learn to bank profits and move on, those will live to fight the next battle. Those who overstay their welcome, or worse, chase parabolic moves, often end up as liquidity for others.

This week’s update leans on that lesson. Momentum is strong, but discipline demands watching the exits. They are as important, if not more important, than the entries.

That sets the tone for this week, hopefully not too long. This is update number fifty-three, covering equities, forex, treasuries, metals, energy, and agricultural commodities, as always with a refreshed summary table and commentary across each market.

Kacper Piotr Kaminski, Cerlogic Markets Research - cerlogic.substack.com

This publication is for informational and educational purposes only and does not constitute investment advice. Markets involve risk, and every participant is responsible for their own decisions.

EQUITY MARKETS – INDICES

$SPX / $SPY, $NDX / $QQQ, $RUT / $IWM, $DAX, $FTSE, $NKD, $HSI, $KWEB

SHORT-TERM TREND CHANGES LAST WEEK:

· FTSE 100 – UNITED KINGDOM: Uptrend 🟩 ➝ Sideways 🟨

COT POSITIONING CHANGES LAST WEEK:

· DOW JONES – UNITED STATES: Neutral 🟨 ➝ Positive 🟩

· NIKKEI YEN – JAPAN: Positive 🟩 ➝ Neutral 🟨

The S&P 500 $SPY is still in “The Big Long.” Passive flows and volatility selling keep the grind higher alive, and until that cycle breaks there is no reason to fight it. The NASDAQ $QQQ rides the same tide, with big tech favorites still carrying the move.

The DOW $DJI is also getting bid. Importantly, this is happening without any real rotation. If it finally comes, the Dow is likely to benefit. At the same time, leveraged funds are starting to lean short, which adds fuel to the move if continue to push higher. The RUSSELL 2000 $IWM remains the most interesting. It is still the index with the most short interest from leveraged funds. If it clears all-time highs, the further squeeze potential is significant.

In developed markets, the MSCI EAFE is still in uptrend, but there are interesting developments under the surface. Up until recently the NIKKEI and the FTSE were doing the heavy lifting, but momentum has changed. The FTSE slipped back into sideways and while the NIKKEI still has BoJ liquidity behind it, but the COT shift to neutral could warn us to watch for signs of fatigue. The DAX is still under pressure from a strong euro, weak industrial demand, and US tariffs. However, at the same time, the new Mercosur trade agreement is a factor to watch. It could create a more durable bid for Germany, and a parallel support European equities more broadly. For now France shows the same pattern as Germany, and lately also Spain, Italy, and Greece are failing to push higher.

China’s Hang Seng $HSI has finally broken out, supported by ongoing stimulus and strong tech flows. US–China trade talks are adding fuel as well. Here, the speculation about a “big deal” is arguably better for markets than an actual deal. If one is signed, it could be a sell-the-news event and spark a moderate correction, but for now the breakout continues. India is still stalling, but we can see strength in broader growth markets. Brazil $EWZ is moving up despite high tariffs, and multiple factors are working in its favor. South Korea $EWY remains one of the strongest performers.

FOREX

$USD, $DXY, $EUR, $AU – GOLD, $CAD, $GBP, $CHF, $BTC

SHORT-TERM TREND CHANGES LAST WEEK:

· CHF/USD – SWISS FRANC: Sideways 🟨 ➝ Uptrend 🟩

· CAD/USD – CANADIAN DOLLAR: Downtrend 🟥 ➝ Sideways 🟨

· ETH/USD – ETHEREUM: Uptrend 🟩 ➝ Sideways 🟨

COT POSITIONING CHANGES LAST WEEK:

· AUD/USD – AUSTRALIAN DOLLAR: Positive 🟩 ➝ Neutral 🟨

The dollar $USD had a wild week around the Fed. Wednesday’s 25 bps cut initially pushed the greenback sharply lower, ran through the stops, and looked like a breakdown. But by Friday the dollar had staged a sharp reversal and reclaimed its critical 97.6 support. That kind of price action is typical at early trend reversal points. Volatility will likely stay elevated into the next few weeks, and the 99.0 resistance remains the key level that could confirm a larger bounce toward 100.0 and 102.0.

Gold $AU remains our core long. The breakout above $3,450 has held, and the setup points toward $3,800. The Swiss franc $CHF has broken into uptrend. It remains the strongest of the majors, despite still digesting heavy US tariffs. Carry trades may unwind if risk assets roll over, which would only add strength to the franc.

The euro $EUR holds steady, supported by partial capital rotation and cheap energy, but capped by weak industrial outlook. This can change with the new Mercosur trade agreement by strengthening broader European positioning globally, however detrimental it could be for the domestic agriculture. Sterling $GBP remains technically improved, but structurally weak with debt and growth headwinds unchanged.

The Japanese yen $JPY remains pinned as the weakest major. The BoJ kept rates unchanged last week and even announced token equity sales. It changes nothing: liquidity support continues, and carry trades remain intact.

The Canadian dollar $CAD has recovered into sideways after its downtrend. The BoC held rates unchanged, and interestingly COT positioning is building for another squeeze higher. Still, oil and mixed commodities keep rallies fragile for now. The Australian dollar $AUD stays in uptrend, but positioning cooled from positive to neutral. The New Zealand dollar $NZD is stuck in sideways, weighed down by low relative rates and soft agricultural prices.

Crypto is mixed. Bitcoin $BTC remains sideways, having reclaimed $112K after shorts were squeezed, it could test recent all-time high. Ethereum $ETH slipped back from uptrend. The $4,100 support and $4,850 resistance are the levels to watch.

The Mercosur deal is also worth mentioning for FX flows outside the majors. Brazil’s Real $BRL could get support from the agreement, alongside the already strong equity bid, making it one of the currencies to keep on the radar.

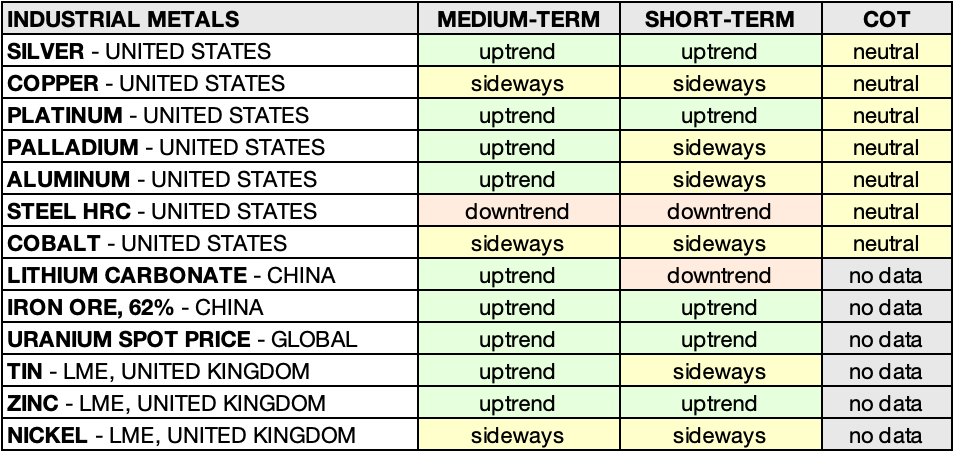

INDUSTRIAL METALS

$SLV, $PL / $PPLT, $PA / $PALL, $HG

SHORT-TERM TREND CHANGES LAST WEEK:

· COPPER – UNITED STATES: Uptrend 🟩 ➝ Sideways 🟨

· PALLADIUM – UNITED STATES: Uptrend 🟩 ➝ Sideways 🟨

· LITHIUM CARBONATE – CHINA: Sideways 🟨 ➝ Downtrend 🟥

· IRON ORE 62% – CHINA: Sideways 🟨 ➝ Uptrend 🟩

· TIN – LME, UNITED KINGDOM: Uptrend 🟩 ➝ Sideways 🟨

· COFFEE C – UNITED STATES: Uptrend 🟩 ➝ Sideways 🟨

Silver $SLV has held its breakout and continues to confirm the upside we had been watching for. We already booked partial profits, and the remainder of the tactical long will be exited if we reach $50. The core position remains intact and will remain so until this bull market is done. If silver pushes higher in a hockey-stick move toward $50, we would expect the market to overshoot that level, attract headlines, pull in late longs, and then engineer a pullback. What happens after that will depend on the fundamental strength of the bull market.

Platinum $PL has regained short-term momentum, moving back into uptrend. We are still long from April, with $1,290 as the risk and exit level. The consolidation phase may be ending, and the next leg higher is setting up. Palladium $PA bounced off $1,100 support all the way to $1,260 resistance, but the follow-through was weak. It has now slipped back into sideways, and the earlier move looks more like relief rally.

Copper $HG is no longer in downtrend. It recovered into sideways on the medium term and briefly pushed into short-term uptrend, but momentum has faded again and it is back to sideways. The distortions from tariffs that had temporarily lifted U.S. prices are gone, and producers are selling into strength. Any sustained recovery still depends on broader industrial demand, which is still missing for now.

Lithium carbonate in China had cooled into sideways after rebounding from peak pessimism, but this week it rolled over into downtrend. Long-term demand still looks likely to exceed current projections, yet near-term patience is required before building positions again.

Uranium continues to hold firm in uptrend across both medium and short-term horizons. Strength is returning, helped by SPUT issuing a large number of new shares. The proceeds will be used to buy more uranium in the spot market, effectively removing supply for years to come. We remain long and patient, awaiting a potential repricing as the contracting cycle and seasonal demand into year-end gather momentum.

Iron ore softened earlier into sideways after Chinese infrastructure support gave it a temporary lift, but has now regained momentum and moved back into uptrend. Tin, which had been firm, lost its uptrend and slipped into sideways. Zinc still holds in uptrend on supply tightness, while nickel has stabilized, moving from downtrend to sideways after testing long-term lows.

ENERGIES

$CL, $NG, $XLE, $COAL

SHORT-TERM TREND CHANGES LAST WEEK:

· NATURAL GAS – UNITED STATES: Downtrend 🟥 ➝ Sideways 🟨

Crude oil $CL has steadied, holding in sideways after last week’s aggressive selling pressure eased. There is a chance the market is building a higher low here, the first step in a bottoming process. Supply remains adequate and demand patchy, which keeps price action choppy in the short term. Structurally, nothing has changed. Years of underinvestment and tighter discipline among producers still argue for much higher prices down the road. For us, this remains a long-term cycle play. We continue to build exposure through oil and gas equities, not as a short-term trade.

Natural gas $NG has moved out of downtrend into sideways. Speculative flows remain light, and momentum is missing, but the long-term demand story through exports to Asia and Europe is unchanged. Sideways is at least an improvement and a reminder that the market is basing out quietly.

Coal $COAL at Newcastle is still under pressure. It lost momentum and moved into downtrend in the short term, while medium-term price action has slipped back to sideways. Margins are squeezed and producers are cutting output. Coal remains one of the most cyclical commodities, and it will offer deep value again, but only once sentiment turns dark enough.

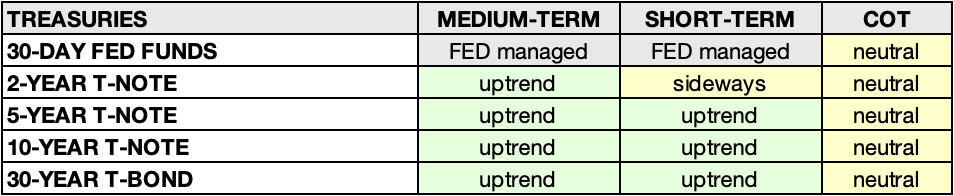

TREASURIES

$SHY, $IEF, $TLT

SHORT-TERM TREND CHANGES LAST WEEK:

· 2-YEAR T-NOTE – UNITED STATES: Uptrend 🟩 ➝ Sideways 🟨

The Fed cut rates by 25 bps last Wednesday. The move sent both the dollar and yields lower, running through stops across the curve. By Friday, however, both had staged sharp reversals. That kind of action is typical at the early stages of a trend reversal, and it leaves us expecting more volatility in the weeks ahead. Paradoxically it’s the 2-year and the 30-year remain sensitive to policy.

We still hold an insurance position in the 2-year, but we are unlikely to increase it here. Inflation may be moving higher from this point, which limits the upside in front-end bonds. The long end is where the real risk sits. Last year the Fed cut rates and yet long yields moved higher, as the 30-year sold off aggressively. That scenario cannot be ruled out again.

The broader theme has not changed. Fiscal dominance keeps duration unattractive, and efforts to manage the curve limit the appeal of owning Treasuries outright. Auctions and inflation prints will guide near-term moves, but the real swing factors remain energy prices, trade policy, and banking regulation.

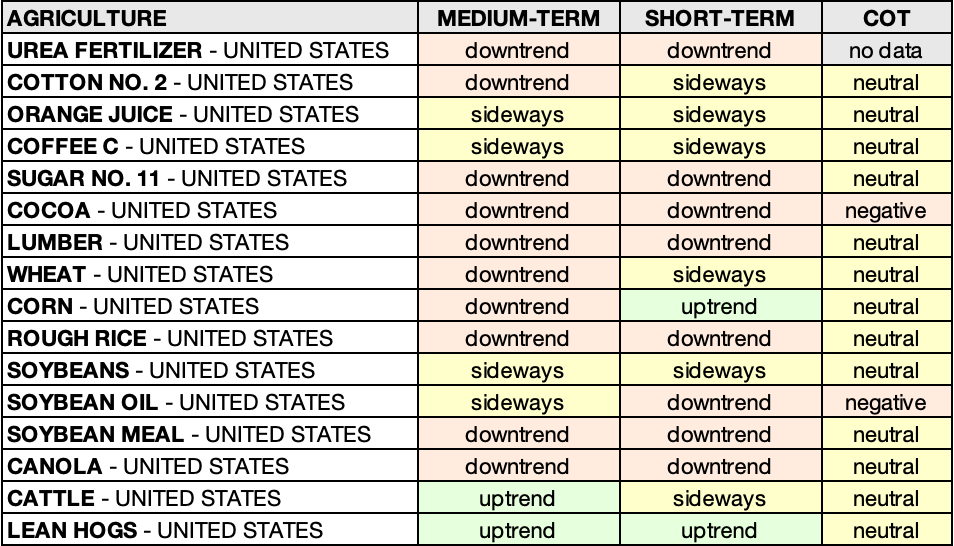

AGRICULTURE

$OJ, $KC, $CC, $LE, $GF, $ZL

SHORT-TERM TREND CHANGES LAST WEEK:

· COFFEE C – UNITED STATES: Uptrend 🟩 ➝ Sideways 🟨

· WHEAT – UNITED STATES: Downtrend 🟥 ➝ Sideways 🟨

· SOYBEAN MEAL – UNITED STATES: Sideways 🟨 ➝ Downtrend 🟥

Coffee $KC has been the standout over the last couple of months, but momentum is finally cooling. After a strong rally driven by tariffs and trade flows, it has slipped back into sideways. The market is still in steep backwardation, and producers have used the spike to sell into strength, which has taken the edge off the move. Cocoa $CC remains heavy, still in downtrend. Producer selling continues and price action looks weak, with no real sign of a base yet. Cotton $CT has stabilized in sideways, trading around production cost levels. Sugar $SB may still be carving out a bottom, but it has more work to do before we can call it. Orange Juice $OJ remains choppy and headline-driven, with no clear signal.

The soybean complex remains fragmented. Soybeans $ZS are still in sideways. Traders continue to watch BRICS trade flows and the possibility of a US–China deal, though that deal looks further away with each week, weighing on sentiment. Soybean Oil $ZL is in downtrend after the short-lived biofuel regulation spike. Soybean Meal $ZM, which had stabilized last week, slipped back into downtrend as selling pressure returned. Canola $RS remains weak and continues to search for a base. Corn $ZC is holding in uptrend after last week’s move higher, and there is no significant producer selling yet. Wheat $ZW has finally recovered into sideways from its long grind lower. A rally of consequence still requires fresh demand, but at least the persistent downtrend has broken.

Protein markets are no longer invincible. Cattle $LE slipped into sideways, with production issues, exports, and tariffed imports still shaping flows. Hogs $HE remain in uptrend, acting as the substitute protein in tariff-distorted trade, even as domestic supply stays ample. Fertilizer prices remain under pressure, with urea in downtrend. That eases input costs for farmers and delays the next inflationary cycle in food commodities.

That’s it for now. As always, reach out if you want to dig into anything further. Below you can find the key economic events this week and important earnings this week I may look at.

Stay safe out there!

Kacper Piotr Kaminski, Cerlogic Markets Research - cerlogic.substack.com

Key Economic Events This Week

Times in GMT -5 / New York Time:

Tuesday, September 23

All Day: 🇯🇵 Holiday – Japan, Autumn Equinox

09:45 🇺🇸 USD: S&P Global Manufacturing PMI (Sep)

09:45 🇺🇸 USD: S&P Global Services PMI (Sep)

12:35 🇺🇸 USD: Fed Chair Powell Speaks

Wednesday, September 24

All Day: 🇿🇦 Holiday – South Africa, Heritage Day

10:00 🇺🇸 USD: New Home Sales (Aug)

10:30 🇺🇸 USD: Crude Oil Inventories

Thursday, September 25

03:30 🇨🇭 CHF: SNB Interest Rate Decision (Q3)

08:30 🇺🇸 USD: Durable Goods Orders (MoM) (Aug)

08:30 🇺🇸 USD: GDP (QoQ) (Q2)

08:30 🇺🇸 USD: Initial Jobless Claims

10:00 🇺🇸 USD: Existing Home Sales (Aug)

Friday, September 26

08:30 🇺🇸 USD: Core PCE Price Index (MoM) (Aug)

08:30 🇺🇸 USD: Core PCE Price Index (YoY) (Aug)

Earnings this week I may look at:

Tuesday, September 23

• Micron Technology $MU US – Technology / Semiconductors

• AutoZone $AZO US – Consumer Discretionary / Retail

• Smiths $SMIN LN – Industrials / Engineering

• Kingfisher $KGF LN – Consumer Discretionary / Retail

• Worthington Industries $WOR US – Industrials / Materials

• AAR $AIR US – Industrials / Aerospace & Defense

• MillerKnoll $MLHR US – Consumer Discretionary / Furnishings

Wednesday, September 24

• Cintas $CTAS US – Industrials / Services

• Paychex $PAYX US – Financials / Services

• Thor Industries $THO US – Consumer Discretionary / Automobiles

• KB Home $KBH US – Consumer Discretionary / Homebuilders

• Enerpac Tool Group $ATU US – Industrials / Machinery

• MFE-MediaForEurope $MS IM – Communication Services / Media

Thursday, September 25

• Costco Wholesale $COST US – Consumer Staples / Retail

• Jabil Circuit $JBL US – Technology / Electronics

• CarMax $KMX US – Consumer Discretionary / Retail

• Vail Resorts $MTN US – Consumer Discretionary / Leisure

• Blackberry $BB CN – Technology / Software

Friday, September 26

• Carnival $CCL US – Consumer Discretionary / Leisure